by Jennifer Riggins

OK maybe it’ll take you more than 20 minutes in the end, but creating a truly agile and actually useful business plan in about an hour ain’t too shabby! Today we go into how to create a down-and-dirty prototype of a business plan to get you moving and to get you focused!

My good friend and fellow guiripreneur John Wolfendale has always shared the desire to work for himself and has been, quite frankly, very good at it, but he hasn’t always been able to express his business strategies very well, when approaching potential business partners or investors. For his first big company that sold £10,000 dance holidays, it took them three years to write a super thick business plan with exec summary, background and history, financials, marketing opportunity, marketing strategy, team, etcetera. He still raised money, but, by the time his business plan—or should we say business tome?—was outdated with his company having pivoted numerous times.

That’s why John, when he was building his current business Eco Vida Homes, was super attracted to the business plan process by Ash Maurya that promises to get you focused on you focused and functional in just 20 minutes. John shared his explanation of this lean change activity with all of us at our annual Writers and Bloggers about Spain conference, and now I’m here to share it with you.

John advised that the video above is about 20 minutes, but you have to pause it often for brainstorming sessions, so time-box yourself for about an hour to focus just on this.

“It’s not perfect—it’s your current thinking that you’re going to test and modify,” he said.

Start-ups that succeed are those that manage to find a plan that works before running out of resources.

Ash Maurya

Step One: Your Customers

John says to make a long list of your current customers. “You’re looking for customer categories that are ‘just right,’ not too broad and not too narrow.” He warns that you need to be careful to distinguish between your “customers” and your “users”—the customers are the ones who pay you. If you have a website or blog, your advertisers are your customers, while your readership are your users.

He says to then pick your strongest customer segment because you’ve got the strongest channel to reach them. “Your success depends on your ability to define your early adopters.”

Step Two: Identify Three Problems

John says your success is based on your ability to define the three problems of your early adopters. For each problem, perform the five-time root-cause analysis, asking “Why is that a problem?” five times for each question. Next ask: How do they solve these problems today? What is their current reality? For each problem, make sure there is a specific solution.

Step Three: Minimal Viable Product (MVP)

“The smallest solution that still delivers customer value. It solves the specific problem and gets you paid,” John explained. If you’re a start-up, survival hinges on you getting that traction.

Step Four: Unique Value Proposition

John calls this creating your finished-story benefit, the end result in a specific time period, where you deal with any objections. He reminded us that this is not set in stone, but rather “This is a guess or a hypothesis, back to the idea that this isn’t a perfect business plan. You can test them and try again.”

Step Five: High Concept Pitch

The high concept pitch is where you distill your unique value proposition into a memorable sound bite,” like “Aliens is like Jaws only in space” or “YouTube is like Flickr for Video.” For John’s own business, it’s: “EcoVida Homes is grand designs without the drama.”

Step Six: Identify Channels

Where are you selling your product or service? Channels are where you communicate your UVP to your customer segments. This can be direct sales through your website or it can be indirect through different sites and resources like Google AdWords or even being mentioned anywhere else. You’re testing your channels from Day One.

Step Seven: Customer Relationships

This is the seemingly simple bit that creates the all-essential customer experience. How do the customers interact with you through the sales lifecycle?

Step Eight: Drive Value

Here’s where you’re producing two metrics. The first is uncovering the customer action that drives value: What do you actually want the customers to do that’s going to create value and get you paid? Now, how many customers do you need to hit that goal?

Step Nine: Pricing and Revenue Streams

John pointed out that pricing is part of your product, offering the common example of how two water bottles can have dramatic pricing differences—which do you respond to emotionally? Which one would you buy? This means that the price has to be relative to the customers’ alternatives, not your costs. “The price determines the customers you attract

Step Ten: Fixed and Variable Costs

Do a rough estimate of your fixed and variable costs in order to determine how many customers you need to break even. How many customers do you need to meet success?

Step Eleven: Key Activities

What ongoing activities do you have to do to continue to increase value for the customer and/or decrease costs for you?

Step Twelve: Key Partnerships

For some companies, these are investors or fully contracted strategic partnerships. For others, it’s simply those people who share aligning but not competing interests where you can help each other out. As best you can, you want to map Key Partnerships to Key Activities, making sure that you are partnering with those that move your objectives forward. Don’t have any key partnerships yet? Then it’s your time to think about what kinds of partnerships you need for which key activities and how you are going to cultivate them.

Step Thirteen: Your Unfair Advantage

What is your unfair advantage? John explains that the mistakes that most people make is thinking that having more features or passion counts here—they aren’t unfair. “Essentially it’s something that cannot be easily copied or bought,” breaking down barriers to entry, like patents, dream teams, celeb endorsements, organic search rankings. He points out that the most likely thing is that you don’t have one. But perhaps it’s just that you don’t know what you have. I mentioned that for our group, the fact that we are all native English speakers in Spain gives us an unfair advantage in the workforce. (In the case of your business, fair is good! If you’re a bootstrapping business, you’ve gotta take all the advantages you can get!)

Step Fourteen: Next Steps

With any business venture, you need to be constantly looking back and thinking forward. Does your business model make sense? Is it competitive enough? Is it attainable? And, is it actionable? What are the next logical steps it leads you to? Does it put you in the right direction?

And if you have business partners or trusted teammates or advisors, what do they think?

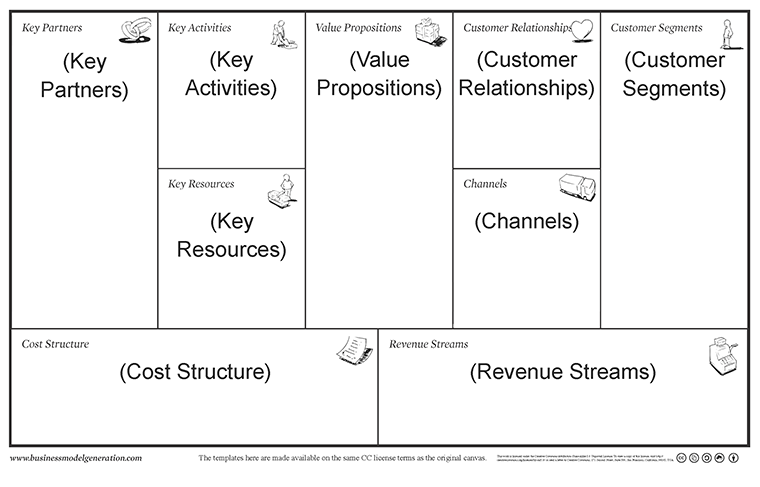

Put it all in a Lean Business Model Canvas

All of these items go into brief bullets in a lean business model canvas, like the one provided by lean coach Alexander Cowan. But don’t worry if it’s not perfect—it shouldn’t be! In fact, this is called lean because it’s just what you need right now, but it comes with the assumption that it’ll change over and over again, just like your business will change, in response to customer needs.

We want to know about your business! Tell us your High Concept Pitch below!

Photo: Unsplash

Awesome. All great reminders and ways to be lean in business. Let me see if I can formulate a high concept pitch is “Networking 3.0 Story Cards are like cue cards for starting dialogue about running a workplace experiment” Yay or nay?